TL;DR — DSR is the list of items with their rates. DAR is the analysis of those rates.

That is the whole difference between the Delhi Schedule of Rates (DSR) and the Delhi Analysis of Rates (DAR). One is a list of items with their rates. The other shows how each of those rates was built.

Simple as that sounds, it is worth going one level deeper, because the moment you have to defend a rate, the difference stops being academic.

Both are published by the Central Public Works Department (CPWD), the body under the Ministry of Housing and Urban Affairs (MoHUA) that issues standard rates for government works. CPWD brings out the DSR and the DAR together, every few years, across Civil Engineering, Electrical & Mechanical Engineering, and Horticulture works.

Here is the difference between the two at a glance:

| DSR | DAR | |

|---|---|---|

| Full form | Delhi Schedule of Rates | Delhi Analysis of Rates |

| What it is | A list of items with finished rates | The analysis behind each rate |

| What it’s used for | Estimates, BOQ, quick lookup | Rate analysis, justification, audit replies |

What the DSR gives you

The DSR is the rate card. Each item gives you four things: code, description, unit, and rate. That is all you need to build a BOQ or an estimate — pick the item, enter your quantity, done.

Two cautions:

- Rates are location dependent

- Rates are time dependent

We will talk about this further in the article.

What the DAR shows you

The DAR is where the rate comes from. For each item, it lists what goes into one unit of finished work — the material, the manpower, and the machinery — each with its quantity and rate, and then the statutory additions (water charges, contractor’s profit & overhead, labour cess, GST) that sit on top.

But a DAR is not a flat list, and this is the part most people underestimate: a DSR item can be built from other DSR items, which are themselves built from more. It is a tree, not a line.

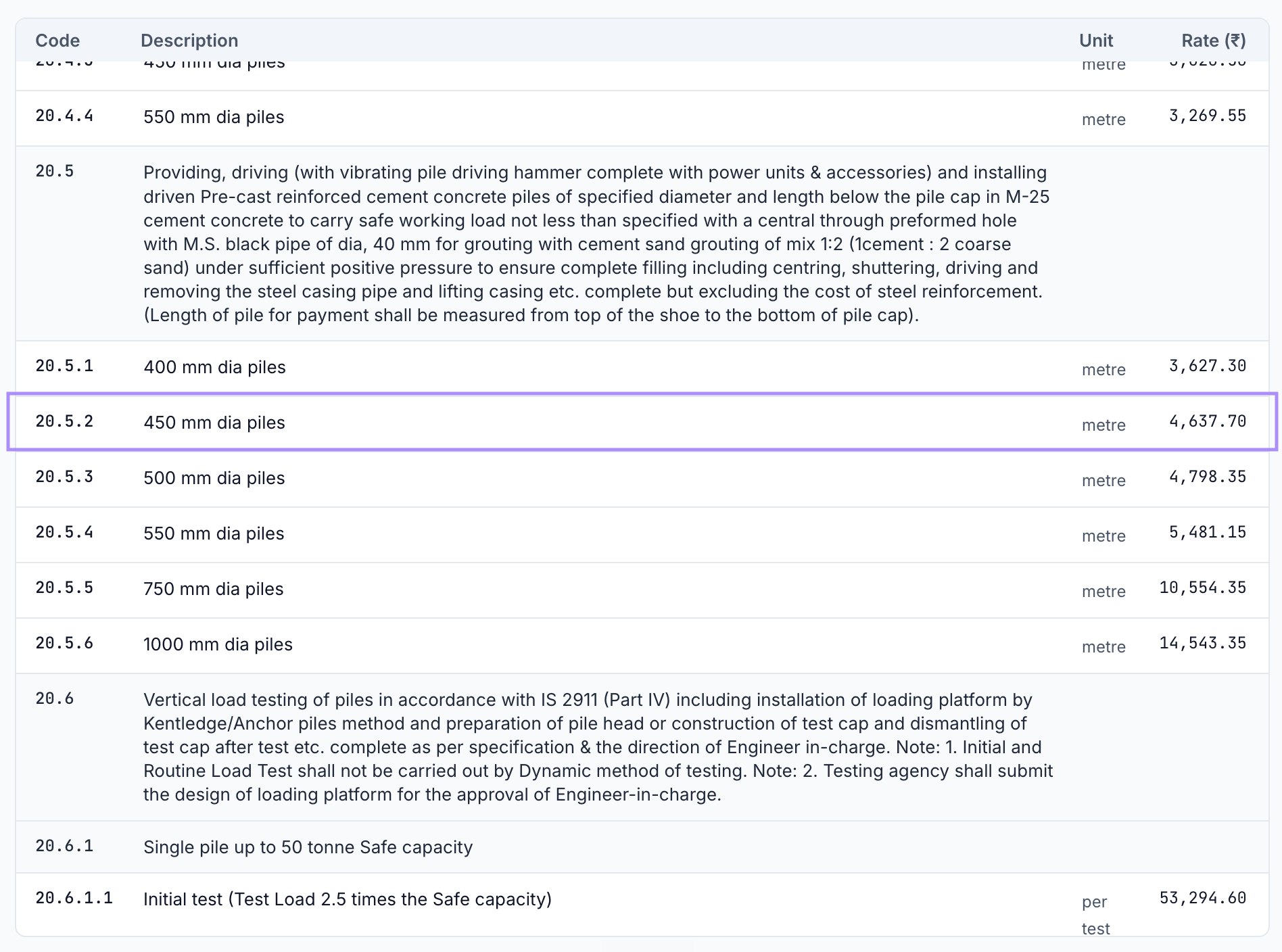

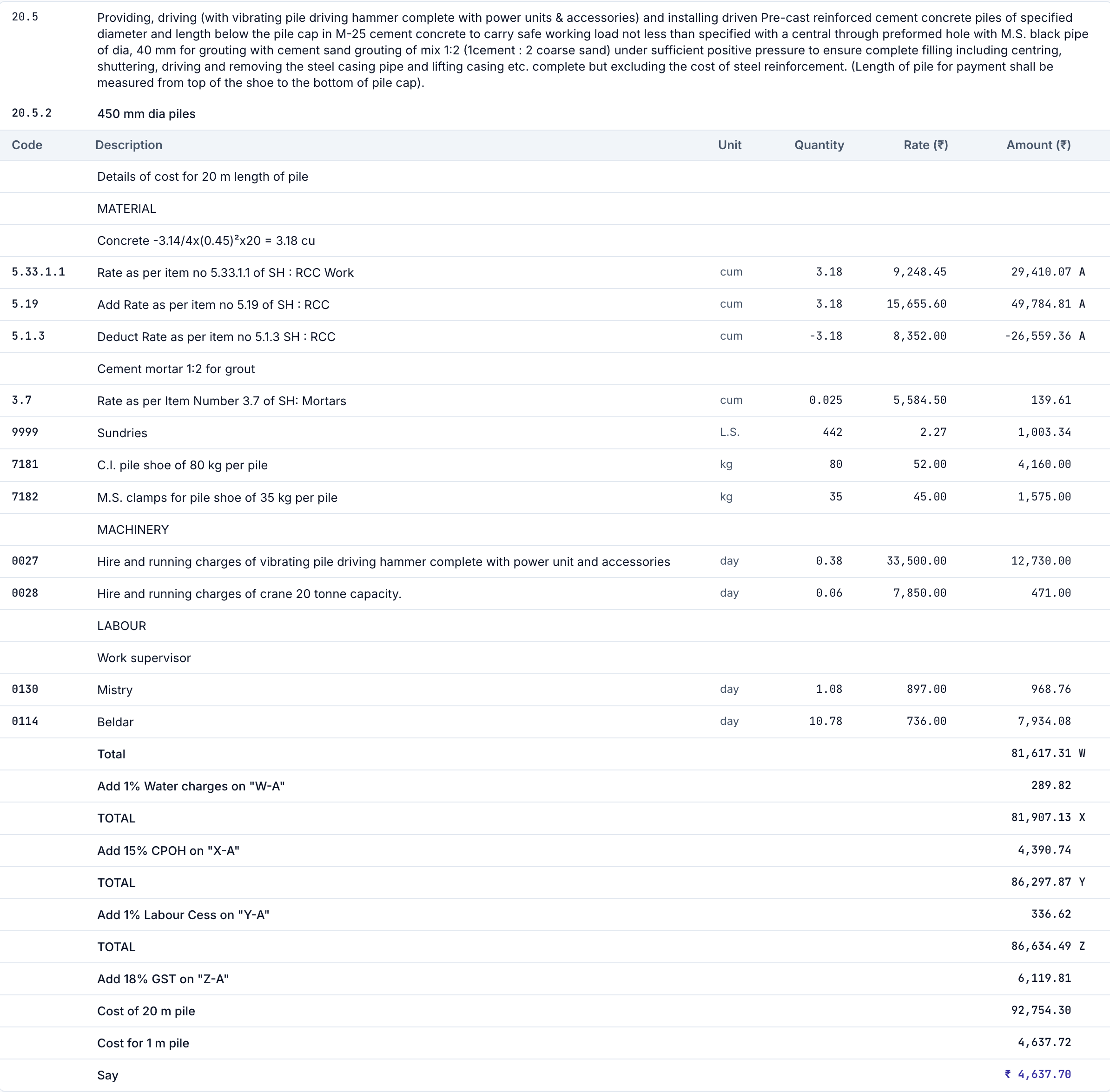

Take item 20.5.2 — 450 mm dia piles, paid per metre. One line in the schedule. Open its analysis and it calls four other DSR items — M25 concrete, encasing steel, 1:2:4 concrete, and cement mortar. One of those calls two more, and that chain runs on: eight nested DSR items, four levels deep. Add up every basic input across that whole tree and you get 81 basic item dependencies, which fold down to 34 unique basic rates — 17 material, 11 manpower, and 6 machinery.

That is why the DAR matters. The printed DSR 2023 lists this pile at ₹4,766.25 per metre — but that one line is really 34 material, manpower, and machinery rates stacked through a four-level tree, and the moment any one of them changes, so does the rate. The figure even depends on which GST methodology you apply (see below). (We pull this single item apart in a separate post; here, the point is just that a DAR is a tree, not a line.)

Costimator is ahead of CPWD’s own rollout — with both methodologies, side by side

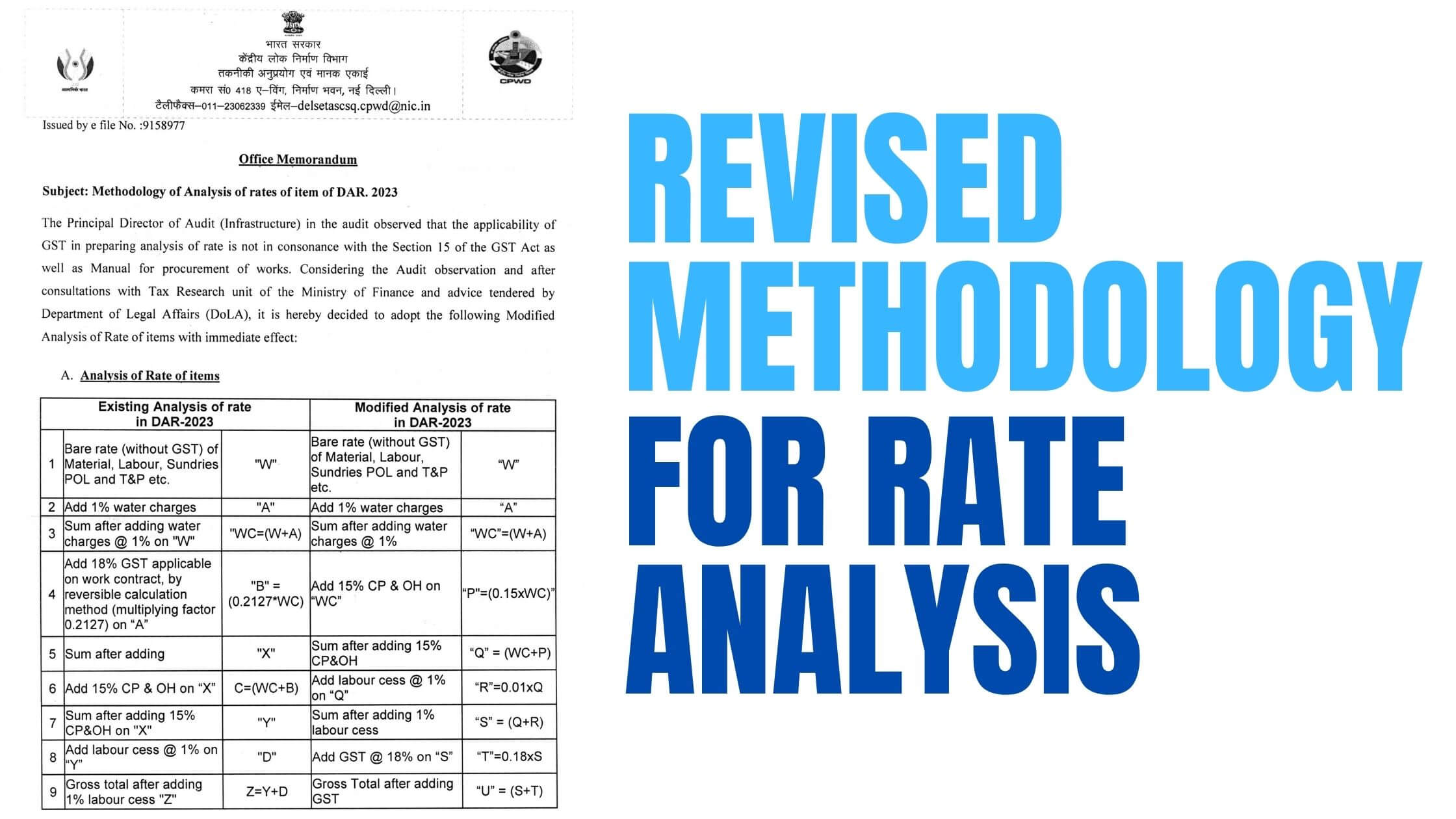

CPWD issued an OM dated 08-08-2024 revising how GST is applied in rate analysis — bringing GST from the older 21.27% compounded factor down to the corrected 18% methodology with Labour Cess now part of the application base. Most engineers are still stuck with the old methodology because CPWD themselves haven’t yet released the updated PDF DSR reflecting this change.

Costimator gives you both. Pick the methodology you need for the current project — classic 21.27% factor to match the existing CPWD PDF, or the OM-compliant 18% factor to stay ahead of the curve. Every rate analysis uses the correct methodology, automatically.

So which one do you use?

Both — it depends on what you are doing.

Use the DSR when you are estimating: a BOQ, an abstract, or a quick scheduled-item lookup. If the item fits your work, the published rate is your reference.

Use the DAR when the rate has to stand up: rate analysis, tender justification, or an audit reply. The DSR gives you the number; the DAR is the only thing that lets you rebuild or defend it.

The catch is that the DSR and DAR are true for exactly one place (Delhi) at one time (the publication year). Your project is almost never both. For a quick estimate elsewhere, you apply a cost index; for a real justification, you rebuild the analysis with current local market rates. Each of those is a topic on its own — detailed guides on the cost index and on market-rate justification are coming next in this series.

FAQ

Why is it called the Delhi Schedule of Rates if CPWD works are all over India?

Because every rate is built on Delhi inputs. For work elsewhere you adjust — a cost index for quick estimates, or a full re-analysis on current local rates when the rate has to be justified.

Are the DSR and DAR published together?

Yes — they are matching CPWD publications for the same cycle. The DSR carries the finished rates; the DAR carries the analysis behind them (Civil, in two volumes each).

Do I need the DAR if I only quote from the DSR?

For a straightforward BOQ on scheduled items, the DSR rate is enough. The moment a rate has to be justified, defended, or rebuilt for local conditions, you need the DAR.

Is the DSR rate enough for audit?

Not on its own, once the rate has to be justified. Audit asks whether the rate is reasonable for the work, the place, and the time — and that is a DAR question, not a DSR one.

The honest problem

Rebuilding even one item’s analysis by hand — chasing every nested item down to its basic rates — is slow. Do it across a 200-item BOQ and it is exactly why files sit unjustified and invite audit observations.

This is what Costimator is built for: pick your items, enter the basic rates once, and it re-analyses the entire tree with your updated market rates — every nested item, every dependency — in seconds.

See it for yourself → explore the features or start a free 14-day trial.

Resources & official sources

Everything on this page is built on CPWD’s own publications. To check any of it against the source: